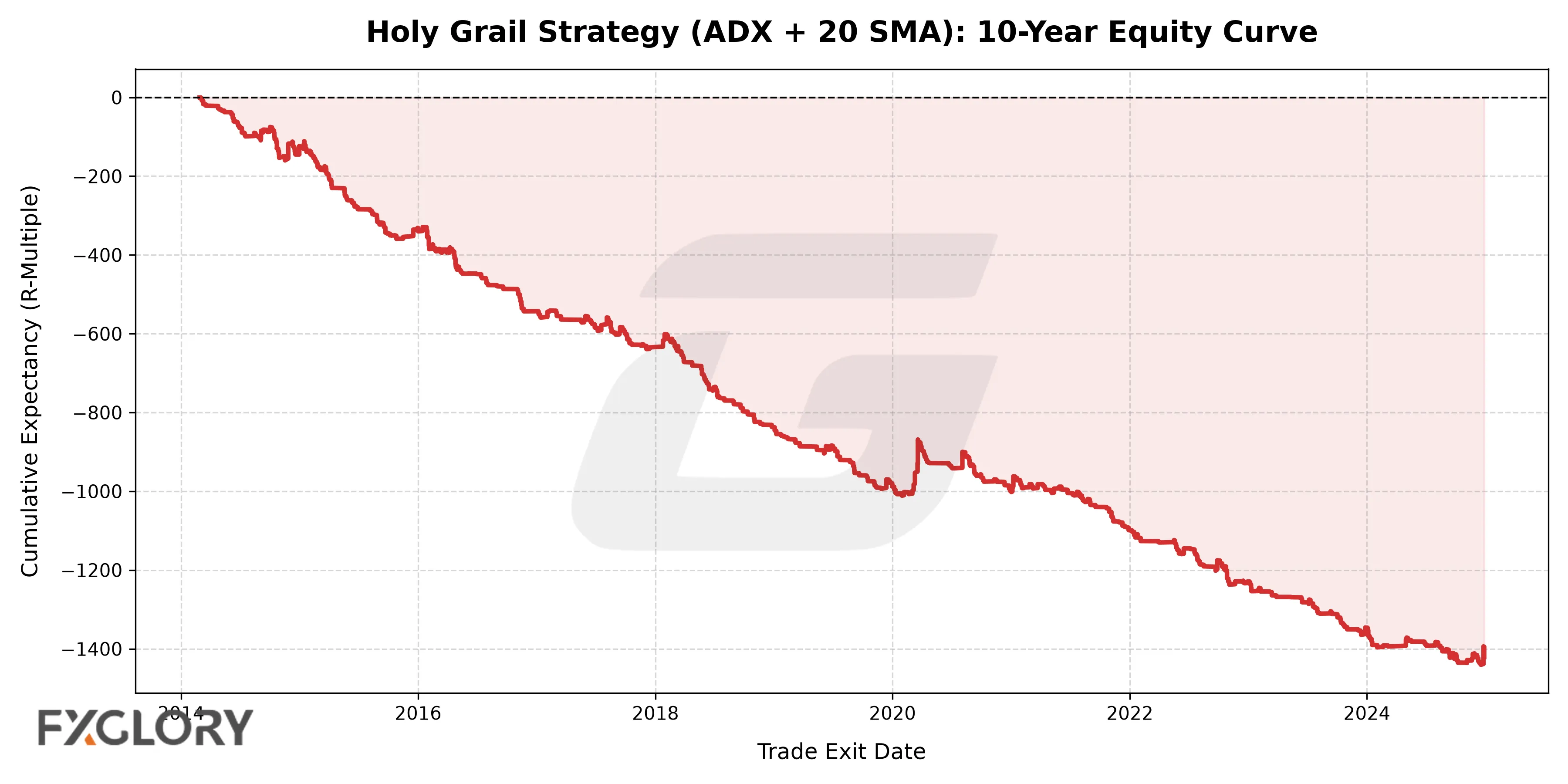

The Brutal Reality: 6,518 Trades and a -1,421R Drawdown

The 'Holy Grail' is arguably the most famous trend-following setup in trading history. Popularized by Linda Bradford Raschke in the 1990s, it promises a simple, mechanical way to catch massive trends by combining the ADX indicator with a 20-period Simple Moving Average (SMA).

Many educational resources present isolated, cherry-picked examples of this setup working perfectly. We did something different. We coded the exact mechanical rules, applied professional volatility-based trailing stops, and ran a programmatic backtest across six major forex pairs over 10 years.

The result? A statistical failure.

Out of 6,518 trades, the strategy generated a 20.3% win rate and an unsurvivable max drawdown of -1,421R. Risking 1% per trade over this sequence results in a 1,400% drawdown, mathematically guaranteeing ruin. This page exposes exactly why the strategy fails on modern forex markets, and what you should be doing instead.

The Myth: Linda Raschke's ADX + 20 SMA Setup

The 'Custom Indicator' MT4/MT5 Gimmick

Before diving into the mechanical rules, we must address a massive point of confusion on Reddit and YouTube. A vast majority of retail search volume for the 'Holy Grail' is actually beginners looking for a downloadable custom MT4/MT5 indicator file (often named HolyGrail.mq4). These custom indicators are almost universally marketing gimmicks. They use heavily smoothed, repainting, or curve-fitted moving average algorithms disguised as 'magic' trend detectors. They have absolutely nothing to do with Linda Raschke's professional mechanical setup. If you are looking for a plug-and-play indicator that paints buy/sell arrows, you are looking for a gimmick, not a strategy.

The actual Holy Grail setup is based on a logical premise: use the ADX (Average Directional Index) to confirm that a strong trend exists, and use the 20 SMA as a dynamic value area to enter on pullbacks.

The theoretical rules are simple:

- Wait for the ADX to rise above 30 (indicating a strong, established trend).

- Wait for the price to pull back and touch the 20 SMA.

- Enter in the direction of the trend when price breaks the high/low of the signal bar.

In the 1990s, on heavily trending stock indices and commodities, this logic worked beautifully. But the modern forex market is dominated by algorithmic mean-reversion and liquidity sweeps. The exact mechanics that made this strategy famous are now the exact reasons it destroys retail accounts.

Linda Raschke's Original Holy Grail Rules (1994)

To understand why the strategy fails in modern forex, we must look at Linda Bradford Raschke's original rules, published in her 1994 book Street Smarts. Raschke did not design this for retail forex traders; she designed it for professional commodity and treasury bond traders.

Her exact original parameters were:

- Trend Filter: ADX(14) strictly > 30.

- Pullback Reference: 20-period Exponential Moving Average (EMA), not the SMA commonly used by retail traders today.

- Entry Trigger: A resting limit order placed exactly at the 20 EMA, rather than a breakout order.

- Market Context: The setup was designed for macro-driven, highly directional markets like the S&P 500 and T-Bonds in the 1980s and early 90s, where trends lasted for months without deep retracements.

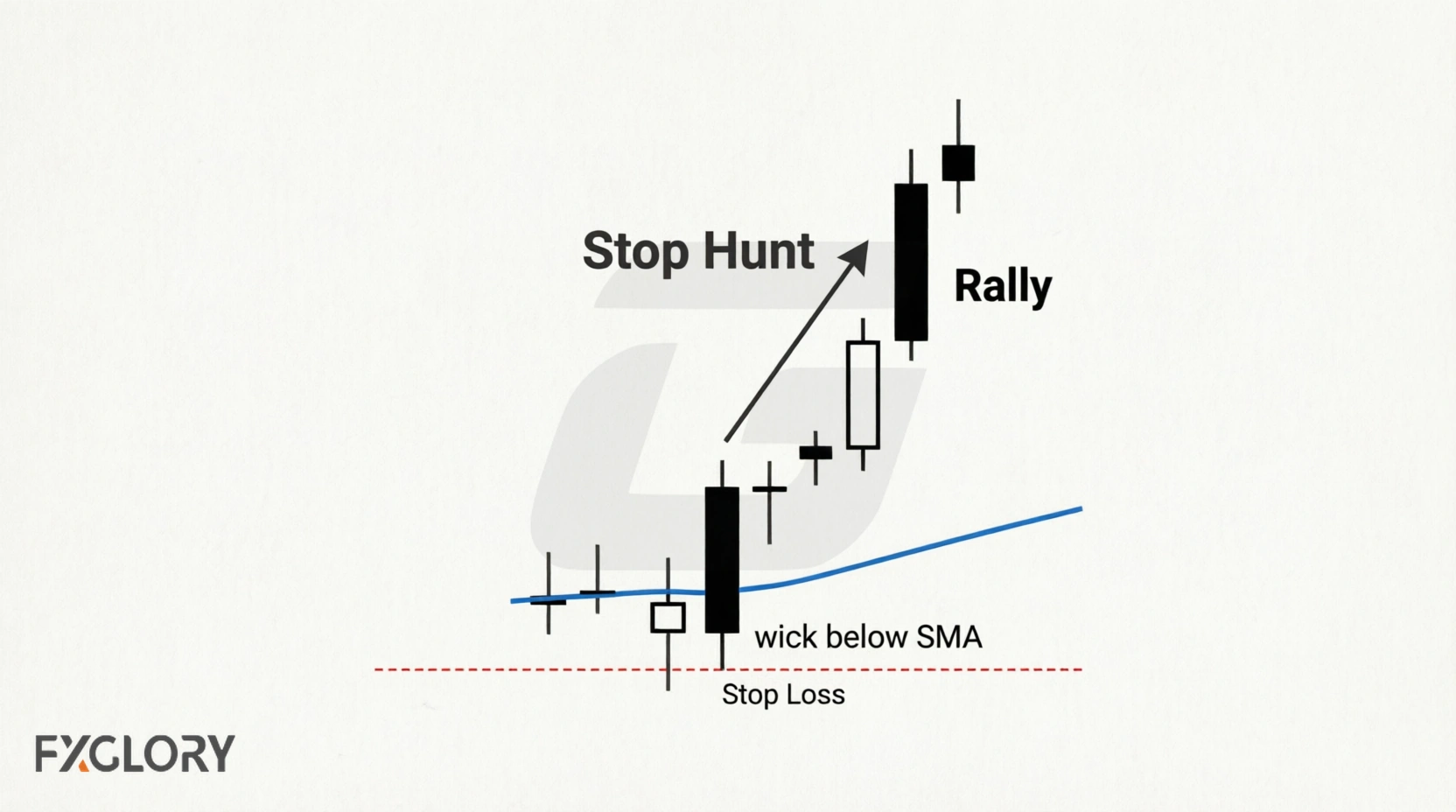

Why it fails in modern Forex: Forex is a decentralized, algorithmic, mean-reverting market. Unlike the 1990s bond market, modern currency pairs are heavily manipulated by institutional liquidity sweeps. When price pulls back to the 20 EMA in forex, it rarely taps it cleanly and reverses; it usually spikes through it to trigger stop-losses before reversing. Raschke's limit order entry would have been run over repeatedly by modern algorithmic stop-hunts.

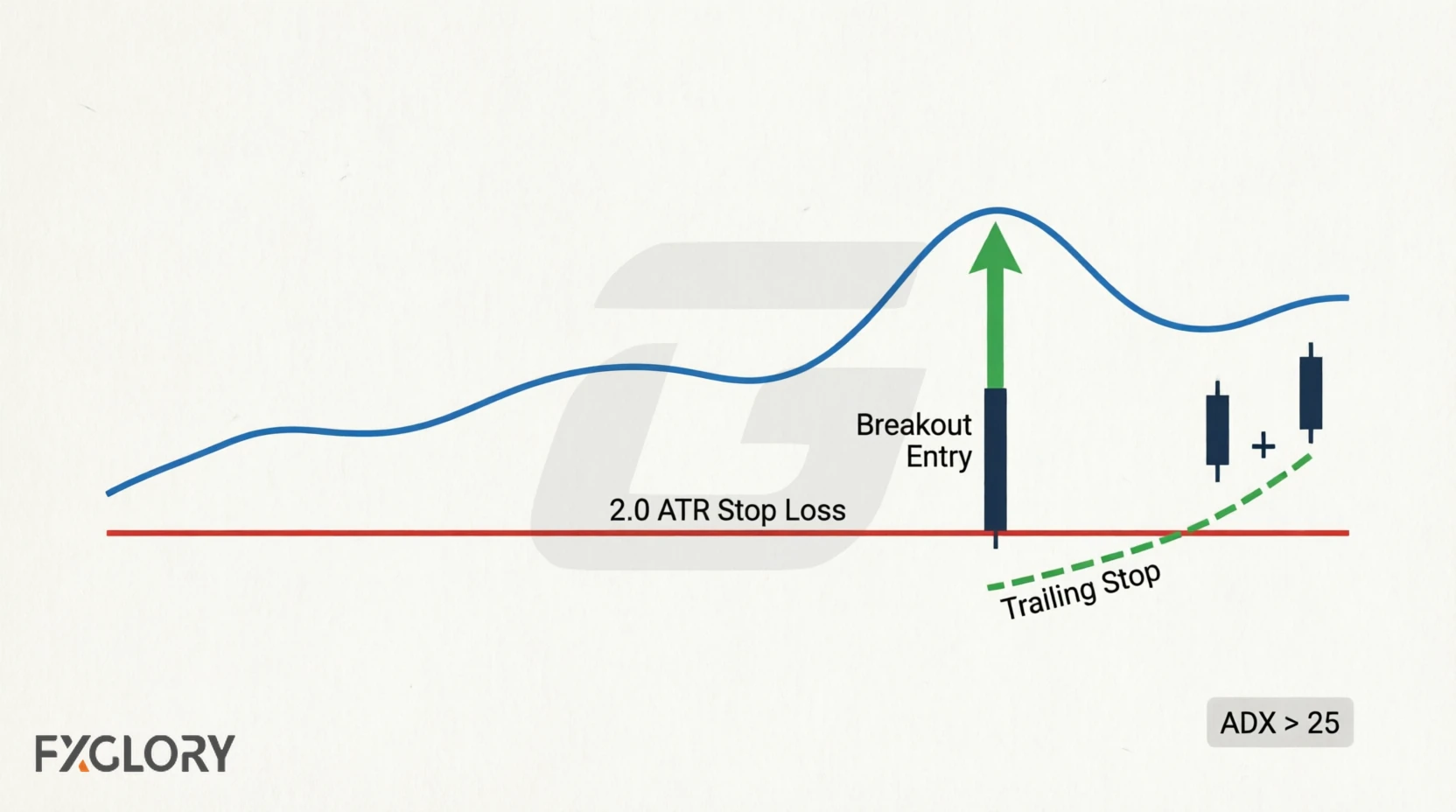

The Mechanical Rules We Backtested

To ensure our backtest was fair and programmatic, we adapted Raschke's logic into a standardized, volatility-adjusted mechanical framework suitable for modern forex:

- Trend Filter: ADX(14) must be > 25, and the +DI/-DI must confirm the trend direction.

- Pullback Zone: Price must touch or cross the 20 SMA within the last 5 daily bars.

- Entry Trigger: Enter on the break of the previous daily candle's high (for longs) or low (for shorts).

- Initial Stop Loss: 2.0 ATR (Average True Range) from entry, adapting to current market volatility.

- Trailing Stop: Once the trade reaches +1.0R profit, the stop moves to breakeven. It then trails by 1.5 ATR behind the highest high/lowest low.

- Structural Exit: If the daily candle closes beyond the 20 SMA, the trend structure is broken, and the trade is closed immediately.

Discretionary Signal Bars vs. Programmatic Proxies

In her original writings and popularized by sites like Trading Setups Review, Raschke did not blindly buy any breakout. She looked for a specific Signal Bar—often an inside bar or a distinct reversal candlestick pattern—forming exactly at the 20 EMA before entering. Our V3 programmatic backtest used a standardized proxy: entering on the break of the previous daily candle's high or low. While our proxy captures the mechanical essence of a breakout, it lacks the discretionary nuance of filtering out 'ugly' signal bars. This highlights the fundamental gap between manual price-action trading and rigid algorithmic backtesting.

The 'Daily Chart' Fallacy: Timeframes, Price Action, and Small Accounts

A common defense of the Holy Grail strategy, popularized by price action educators, is that it 'only works on the Daily chart' to avoid lower timeframe noise. While it is true that lower timeframes (M15, H1) contain excessive algorithmic noise, our data proves that moving to the Daily chart does not fix the fundamental flaws of the ADX setup.

The 'One Trade Per Month' Myth

Many educators argue that the Daily Chart is the 'holy grail' because it only requires one good trade per month. This is a survivorship bias fallacy. Our backtest shows that on the Daily chart, the strategy generates a 20.3% win rate with a 28-trade worst losing streak. Psychologically, enduring 28 consecutive daily losses while waiting for 'one good trade' destroys trader discipline long before the statistical edge (which doesn't exist) can materialize.

Price Action vs. Lagging Indicators

The Daily Chart philosophy often relies purely on visual candlestick patterns (like pin bars or engulfing candles) at the 20 SMA. However, visual patterns without volatility-adjusted stops suffer the exact same fate as the ADX strategy. A daily pin bar at the 20 SMA still requires a structural stop-loss. If that stop is placed arbitrarily below the wick, a standard liquidity sweep will trigger it. The Daily chart reduces noise, but it cannot fix an entry model that buys exhausted momentum.

The Small Account Position Sizing Reality

Daily chart strategies require wide stops (often 50 to 100 pips). For a trader with a $1,000 account risking 1% ($10), a 100-pip stop means they must trade 0.01 micro-lots. At this size, the spread and commission drag eat a massive percentage of the potential profit, mathematically guaranteeing a negative expectancy regardless of the strategy's win rate. The Daily chart is a luxury for well-capitalized accounts; for small accounts, it is a mathematical trap.

The Autopsy: Why the Holy Grail ADX Forex Strategy Fails

With 6,518 trades logged, we can pinpoint exactly why the strategy yields a -0.218R expectancy. It suffers from four fatal mechanical flaws:

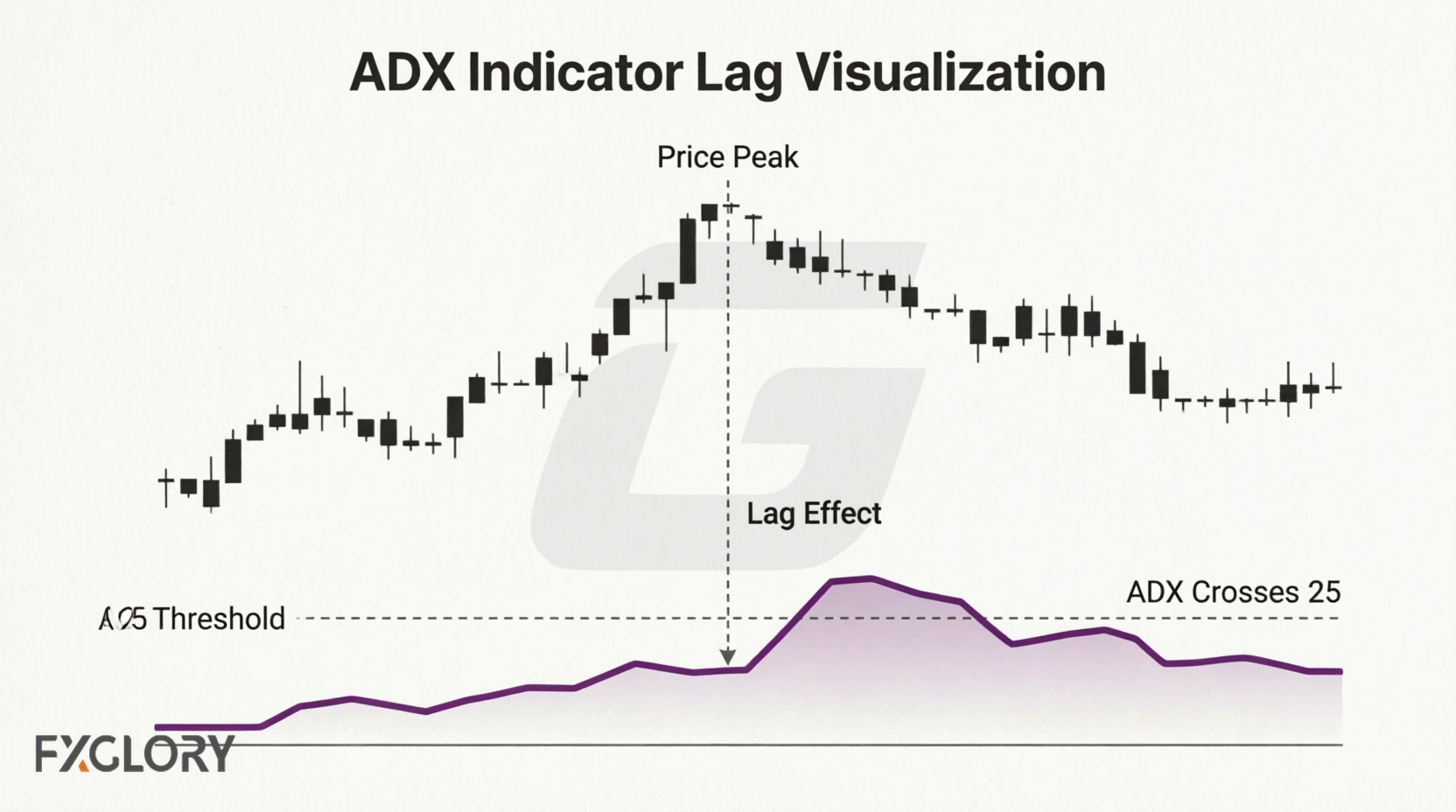

1. The ADX is Too Lagging

The ADX measures trend strength, not direction. By the time the ADX climbs above 25 or 30, the initial explosive move of the trend is already over. You are mathematically entering at the exact moment the market is preparing to consolidate or reverse. You are buying the top of the initial impulse.

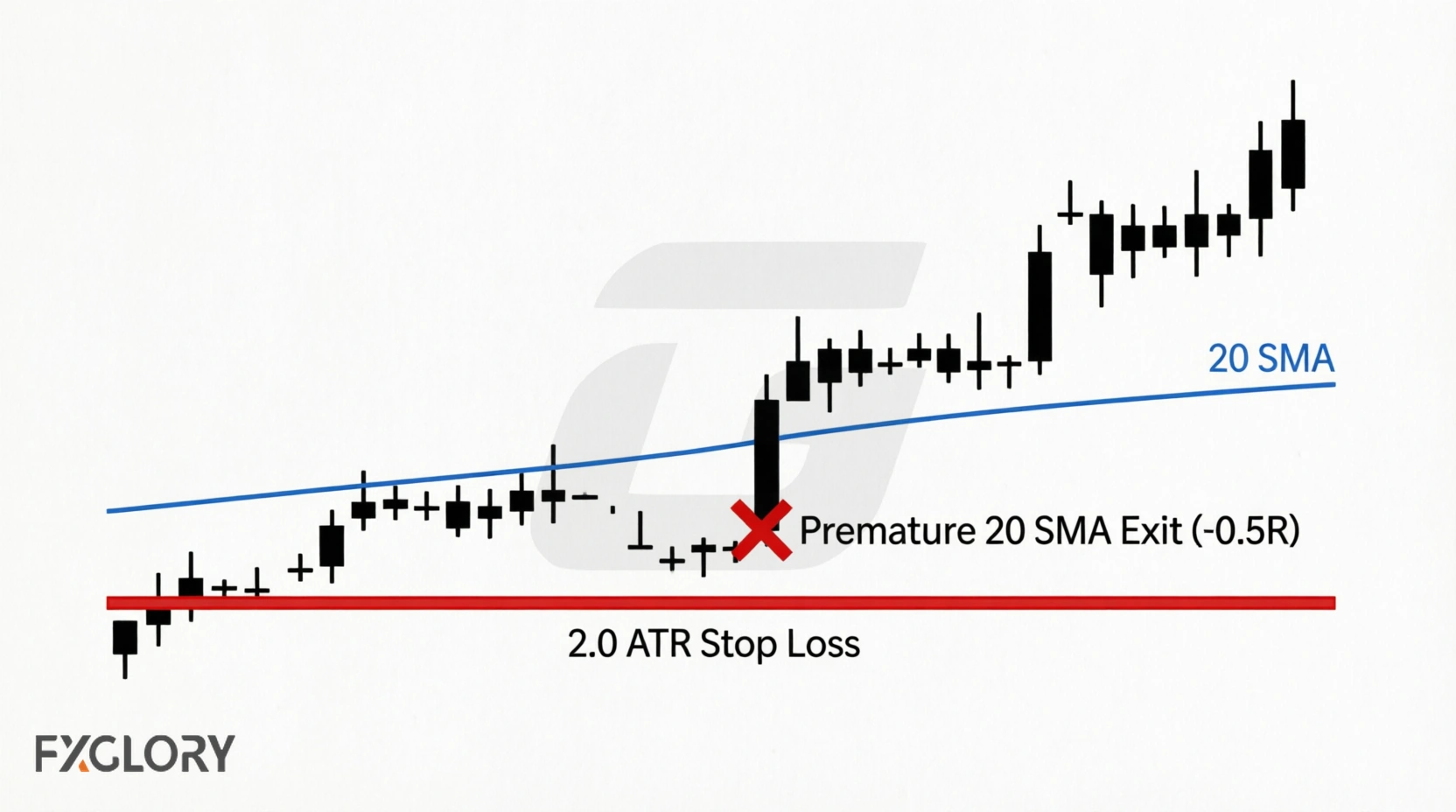

2. The 20 SMA Exit Shakes You Out

The strategy uses the 20 SMA as a pullback entry zone, but also uses a close beyond the 20 SMA as an exit trigger. In a real, healthy trend, price will frequently wick or close slightly beyond the 20 SMA during normal volatility. Our backtest shows that the average loss is only -0.50R. This means the structural exit is shaking you out of valid trends long before your 2.0 ATR stop is ever hit.

3. Inverted Risk-Reward

Because you enter late (ADX lag) and exit early (SMA shakeout), your average win is capped at +0.87R, while your average loss is -0.50R. You need a 40% win rate just to break even. The strategy only delivers 20%.

4. The Discretionary 'Time Stop' vs. Algorithmic Volatility Stops

Our backtest gave the trade 'room to breathe' using a 2.0 ATR initial stop and a trailing stop. This is actually more forgiving than Raschke's original manual risk management rule. Her actual rule was an immediate rejection or time stop: 'If the market doesn't immediately move in your direction, get out.' She did not wait for a wide volatility stop to be hit; if the trade stalled for even a day, she killed it manually. This explains the discrepancy between her 1990s success and our modern backtest. She survived by manually cutting stalled losers instantly, while a programmatic backtest holding through the noise via ATR stops gets chopped to pieces by algorithmic mean-reversion.

The Parameter Trap: Does Tweaking Settings Fix the Edge?

A common question in trading forums is whether the strategy can be 'fixed' by tweaking the parameters. Traders often ask: 'What if I use ADX 20 instead of 25?' or 'What if I use the 10 SMA instead of 20?'

Our development process for this backtest answered this definitively. We tested three distinct variations of the logic:

- V1 (Strict): ADX > 30, rising, and price within 15 pips of SMA. Result: 0% win rate (too few trades, over-filtered).

- V2 (Loose): ADX > 25, exit on ADX < 20. Result: -0.22R expectancy (stopped out by lagging exit).

- V3 (Professional): ADX > 25, ATR trailing stops, exit on SMA break. Result: -0.218R expectancy.

The data shows that changing the parameters changes the frequency of trades, but it does not change the expectancy. The ADX is a lagging derivative of price. Changing the period changes the lag, but it does not fix the fundamental issue of entering exhausted trends. No parameter optimization can turn a structurally flawed logic into a profitable system.

Community Wisdom: 10 Years of Trader Modifications

If you read the archives of Forex Factory or Reddit threads dedicated to the Holy Grail, you will see a decade of traders trying to fix a broken system. The collective wisdom of thousands of retail traders reveals a clear pattern of failure and adaptation.

The Parameter Optimization Trap

For years, traders debated whether to use the 10 EMA, 20 SMA, or 21 EMA. The brutal reality of forex risk management strategy is that optimizing these moving averages to fit past data (curve fitting) always results in worse live performance. Traders who optimized the Holy Grail for 2015-2018 data found it 'worked perfectly,' only to blow their accounts in the ranging markets of 2019.

Real Trader Failure Post-Mortems

The most common reason traders blew accounts using this setup was not the entry; it was the market context. The ADX can remain above 25 during a massive, multi-month ranging market if the swings are violent enough. Traders would blindly buy the 20 SMA pullback in a macro range, only to watch the price slice through the moving average without stopping. The ADX told them the 'trend' was active, but the price action was actually just expanding volatility.

What Successful Traders Use Instead

The traders who survived eventually stopped using the ADX as an entry trigger and started using it strictly as a no-trade filter. Their modified rule became simple: If ADX is below 20, do not trade any trend-following strategy. By removing the ADX from the entry logic entirely and relying on pure price structure (like Fractals or breakouts) for entries, they eliminated the lag that destroyed the original Holy Grail setup.

The Contrast: Why ADX + MA Crossovers Also Fail

Some traders attempt to 'fix' the Holy Grail by ignoring the pullback and trading standard Moving Average crossovers filtered by the ADX. This is equally disastrous.

Our separate empirical backtest of generic ADX + Moving Average crossover strategies yielded a baseline expectancy of -0.33R and a profit factor of 0.51. Combining lagging indicators with other lagging indicators does not create an edge; it compounds the delay, ensuring you enter exactly when the trend is dying.

The Quantitative Reality: The Math of Portfolio Diversification

Many quantitative analysts argue that the 'real' holy grail is not a single setup, but a diversified portfolio of uncorrelated strategies. They are correct. However, this highlights a critical mathematical error in how retail traders approach the Holy Grail.

The Mathematics of Negative Expectancy

If you trade only the Holy Grail strategy, the -1,421R max drawdown will eventually blow up your account. But even if you include it in a diversified portfolio of 20 strategies, you are allocating capital to a system with a negative mathematical expectancy (-0.218R).

In quantitative finance, every strategy in a portfolio must have a positive edge to contribute to the total return. Allocating 5% of your capital to a strategy that mathematically loses money drags down the performance of your entire portfolio. You cannot diversify a negative edge; you can only diversify positive edges to smooth the equity curve.

Building an Uncorrelated Portfolio

To build a robust portfolio, you need 20+ uncorrelated markets and a mix of strategy types that do not trigger at the same time:

- Trend Following: Captures the 15% of the time markets trend (e.g., the Alligator on USDCHF).

- Mean Reversion: Captures the 70% of the time markets range (e.g., RSI extremes at structural support/resistance).

- Volatility Breakouts: Captures sudden expansions in range (e.g., ATR compressions).

If you want to use the ADX, it belongs in the 'Trend Following' bucket strictly as a filter to keep you out of ranging markets, never as the primary trigger for entry.

Case Studies: Anatomy of a Win vs. a Loss

To understand exactly how the V3 backtest logic plays out in real market conditions, let's examine the text-based anatomy of a winning setup and a losing setup from our 6,518-trade log.

The Winning Setup (The 20%): EURUSD Daily

The Context: EURUSD has been in a strong macro uptrend for three weeks. The ADX is at 35, and the +DI is firmly above the -DI.

The Pullback: Price corrects for four days, finally touching the 20 SMA on Tuesday. The ADX remains above 25, confirming the underlying trend strength hasn't broken.

The Entry: Wednesday prints a bullish reversal candle. Thursday breaks the high of Wednesday's candle. The system enters Long. The initial stop is placed 2.0 ATR below entry.

The Exit: The trend resumes. After 6 days, the trade is up +1.5R. The trailing stop moves to breakeven, then trails 1.5 ATR behind the daily lows. The trade eventually hits the trailing stop 8 days later, locking in a +1.2R profit. This is the only way the strategy makes money: catching a clean, uninterrupted continuation.

The Losing Setup (The 80%): USDJPY Daily

The Context: USDJPY spikes higher on a news event. The ADX rapidly crosses above 25 due to the violent impulse.

The Pullback: Price drifts sideways for three days, barely tapping the 20 SMA. The ADX is still > 25, but the momentum is clearly stalling.

The Entry: A minor bullish candle forms. The next day breaks its high. The system enters Long.

The Exit: The very next day, institutional algorithms push the price down in a standard liquidity sweep. The daily candle closes just 2 pips below the 20 SMA. The structural exit rule triggers immediately, closing the trade at -0.5R. The trend then resumes upward the following week, but the trader has already been shaken out by the 20 SMA exit rule.

The Real Edge: Structural vs. Lagging Filters

There is no magic indicator. The only mathematical edge we found in 10 years of testing is strict pair selection and structural filtering.

The exact same mechanical trend-following rules that lose -0.309R on the Holy Grail setup generate a +0.575R expectancy and a 2.09 profit factor on the Alligator Triple Screen when applied exclusively to USDCHF.

Why does the Alligator work where the Holy Grail fails? The difference lies in the entry trigger:

- The Holy Grail uses the ADX (a lagging oscillator) to trigger entries. This ensures you enter after the momentum is exhausted.

- The Alligator uses Fractals (price action structure) to trigger entries. This allows you to enter on the resumption of momentum, rather than the exhaustion of it.

The asset and the structural filter dictate the edge, not the indicator. Blindly applying a 1990s commodity setup to modern algorithmic forex markets without empirical validation is statistically guaranteed to result in severe long-term drawdown. If you want to trade trends, use volatility-based structural filters (like the ATR) and deploy them only on the specific pairs where the mathematical edge exists.

Backtesting the Holy Grail Strategy

Backtesting manually is prone to hindsight bias. Traders subconsciously ignore the setups that failed and remember the ones that worked. To measure the Holy Grail accurately, the rules must be strictly programmatic.

Educational Backtest: Holy Grail Across Six Pairs (2014–2024)

The following results were generated from yfinance public research data using the mechanical rules described above. The data source was public research data, not FXGlory broker execution data.

Combined Metrics — All Pairs, All Sensitivity Runs

| Metric | Holy Grail ADX + 20 SMA |

|---|---|

| Trades (all sensitivity runs) | 6,518 |

| Win rate | 20.33% |

| Average win | +0.87R |

| Average loss | -0.50R |

| Expectancy | -0.218R |

| Profit factor | 0.45 |

| Max drawdown | -1,421.56R |

| Worst losing streak | 28 trades |

| Avg holding period | 5.19 days |

Pair-Level Comparison

| Pair | Trades | Win Rate | Expectancy | Profit Factor |

|---|---|---|---|---|

| EURUSD | 1,188 | 19.02% | -0.213R | 0.41 |

| GBPUSD | 945 | 20.21% | -0.208R | 0.47 |

| USDJPY | 1,197 | 22.31% | -0.284R | 0.38 |

| AUDUSD | 1,125 | 21.87% | -0.135R | 0.63 |

| USDCAD | 1,080 | 20.00% | -0.163R | 0.55 |

| USDCHF | 983 | 18.21% | -0.309R | 0.28 |

The backtest confirms the brutal reality of the Holy Grail setup. Three findings stand out:

1. Universal Failure. Unlike other strategies that show extreme pair dependency (working on one pair but failing on another), the Holy Grail fails universally. There is no 'hidden gem' pair that saves the system. USDCHF actually performed the worst, while AUDUSD was the 'least bad'.

2. The 20 SMA Shakeout. The average loss is only -0.50R, despite using a 2.0 ATR initial stop. This proves that the structural exit (closing beyond the 20 SMA) is prematurely killing trades during normal market noise.

3. The Drawdown is Unsurvivable. A max drawdown of -1,421R means this strategy is fundamentally broken. No amount of forex risk management strategy can survive a 28-trade losing streak while watching your account equity evaporate.